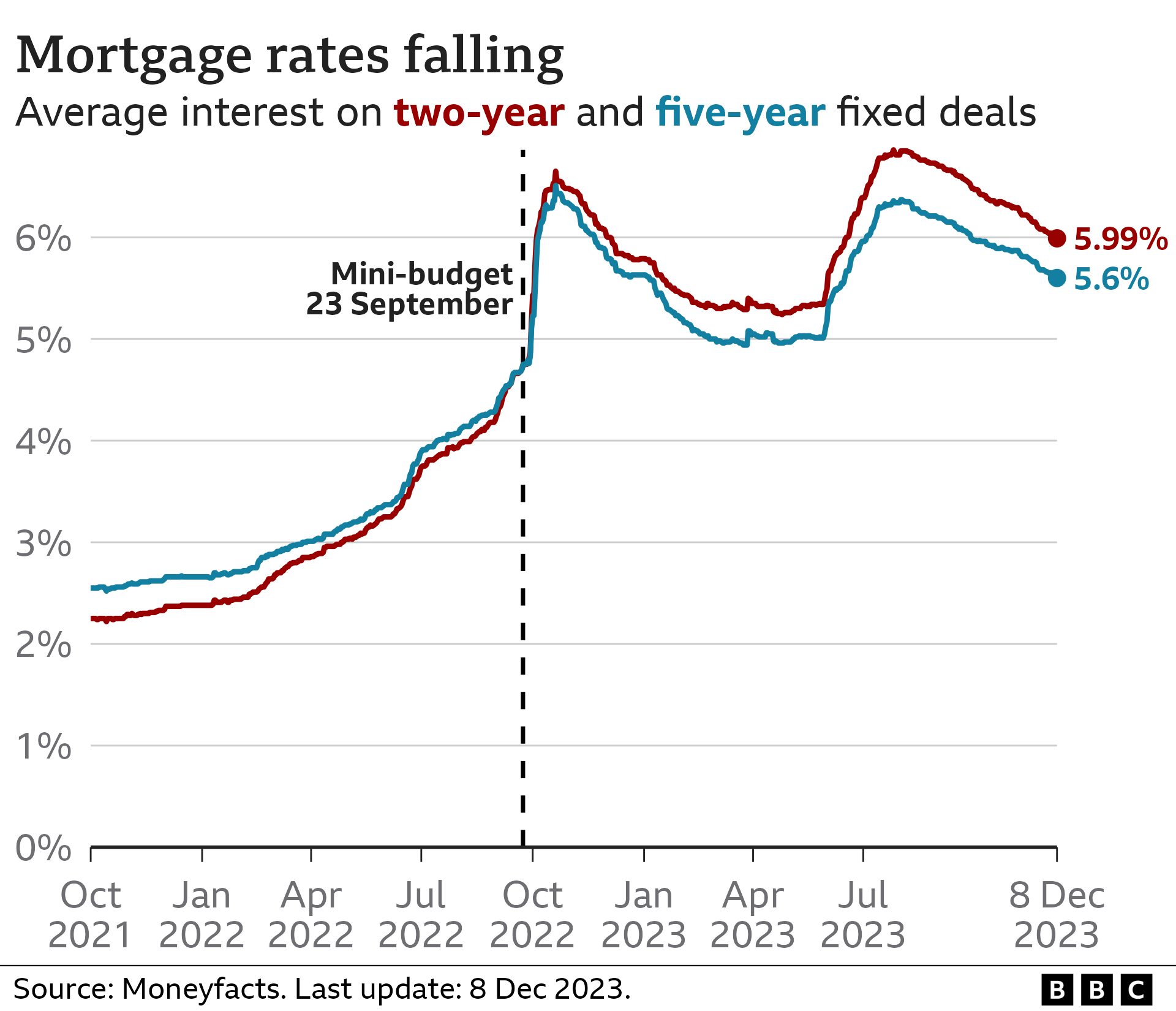

Mortgage rates on a typical two-year fixed deal have fallen below 6% for the first time since mid-June, according to Moneyfacts.

The financial information service said the average rate was now 5.99%.

Competition among providers has intensified as they face a battle to attract a small pot of new homeowners, and to maintain current custom.

They have been given added confidence as many analysts suggest the Bank of England’s base rate has now peaked.

The rate on a typical two-year fixed mortgage rose sharply during Liz Truss’s premiership, then fell slightly before rising again.

It peaked at 6.86% in late July, and has been falling steadily since.

David Hollingworth, from broker L&C Mortgages, said that the best rates for two-year fixed deals were below 5%, or under 4.5% for five-year deals.

However, this was still significantly higher than many homeowners paid for more than a decade, and many of these deals were close to their end date.

The Bank of England’s latest Financial Stability Report estimated five million mortgage holders would see their mortgage payments rise by 2026.

According to the Bank’s estimates, just under 900,000 will see mortgage payments jump by more than £500 a month due to higher interest rates.

About a fifth of those are predicted to see a jump of more than £1,000 per month.

But the number of households predicted to spend more than 70% of their post-tax income on their mortgage by the end of next year has fallen to 500,000 from the 650,000 predicted in July.

Mr Hollingworth said some lenders may have “overshot” when setting their mortgage rates during the summer as the Bank rate was rising. It has now been held twice at 5.25%.

He said mortgage rates were now at more historical norms, but would still be painful after years at a low level. Many were choosing a two-year, rather that a five-year, deal in the hope rates would fall further, although there were no guarantees of that scenario.

He suggested people searching for a new mortgage prepare early, lock in a product that suits them, then review before their current deal expires.

“The danger is not to do anything,” he said, pointing out that default standard variable rates were often very expensive.